How do I defend a dispute?

Find out how to defend a dispute.

How do I defend a dispute?

The reason code categories for disputes raised by cardholders determine whether you have a chance to defend the dispute or if it will result in an automatic chargeback. Always adhere to the instructions from Wpay regarding retrievals or chargebacks and submit your responses by the specified deadlines.

When you seek to challenge a dispute, provide as much detail as possible to support your case and increase the chances of a positive outcome.

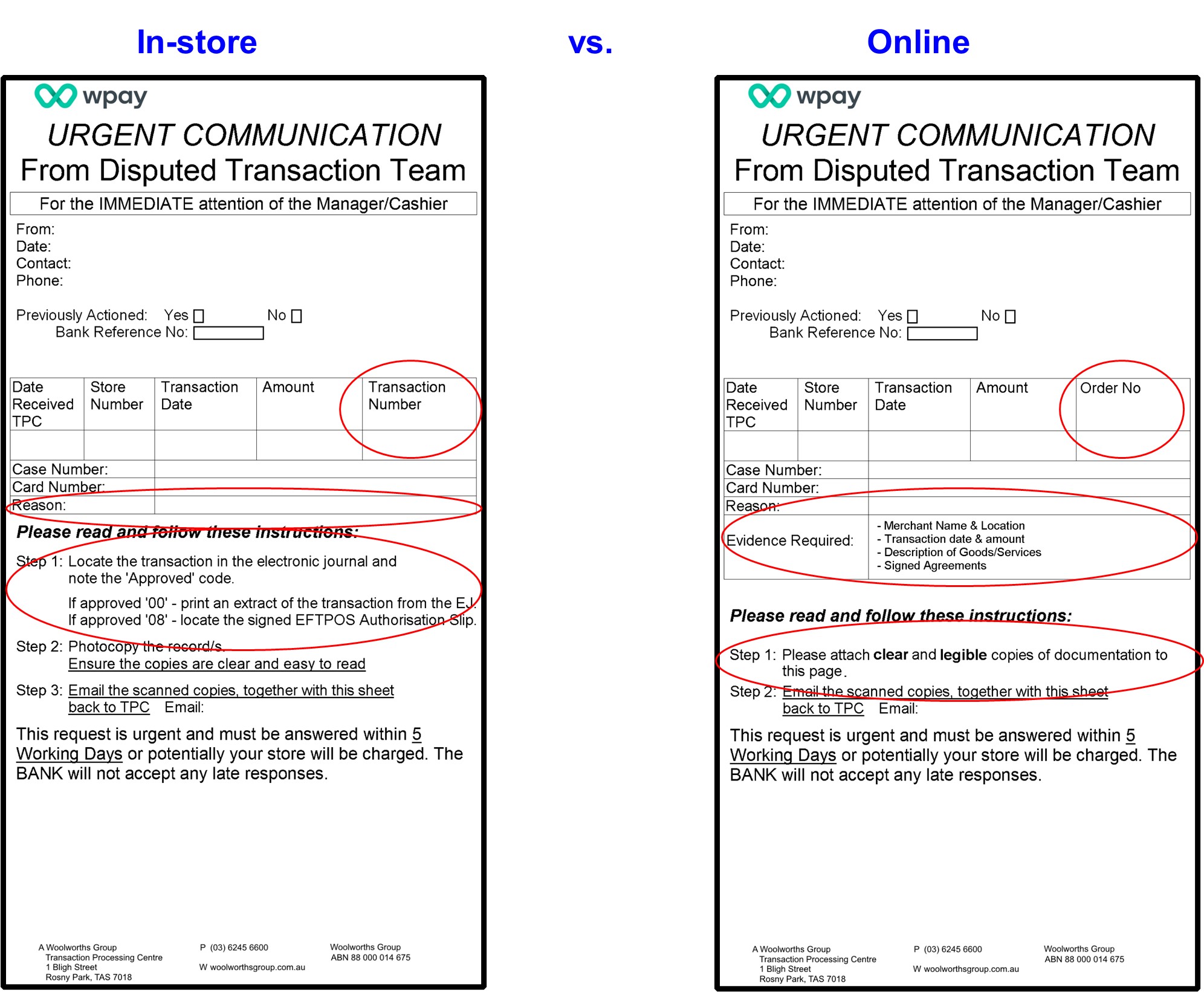

An email will be sent to your merchant’s email address or in the case of sub-merchants being serviced by a Payfac, the email will be sent to the Payfac’s email address. The merchant or sub-merchant (in the case of Payfac) should send their response to the Dispute Resolution Team contact details ([email protected]).

Example of email notification

Please consult the relevant Scheme guides (see Scheme links below) for the complete list of dispute reason codes and suggested evidence to challenge a dispute effectively.

Detailed below are common dispute reasons and suggested evidence to respond with..

For Card Present transaction disputes

| Dispute Reason | Description | Required actions |

|---|---|---|

| - No Authorisation - Fraud - Declined Authorisation - Copy of Authority - Counterfeit Fraud | A customer is claiming they did not authorise or participate in a transaction that was processed at your store. This could be the result of: - A customer’s stolen credit card was used to make the purchase; - The customer does not recognise the transaction on their statement or does not remember shopping on that day. | Obtain a copy of the invoice/receipt for the transaction and forward it to the Disputes Resolution Team. For Store And Forward (SAF) transactions, ensure to include a signed copy of the receipt. |

| - Duplicate Processing | A customer is claiming that they were charged twice or more for a transaction at your store. This could be the result of: - A customer not recognising a second purchase made on the same day or on a weekend for the same dollar amount and now appearing on their bank statement as two transactions for the same value on the same date. - A Wpay back end payments issue whereby a customers card was debited directly | - Review the invoice/receipt for each transaction and verify whether it was two separate transactions or if the customer had actually been charged twice. - If the customer was charged twice, send evidence to the Disputes Team confirming the chargeback was valid. - If it’s not a duplicate transaction, obtain a full copy of the invoice/receipts for both of the disputed transactions and send them to the Disputes Team. If a credit or reversal for the transaction has been processed, please provide documentation indicating the amount and date of the credit/reversal. |

| - Incorrect Amount | The customer submitted a dispute to their bank that claims: - The transaction amount is incorrect. - An addition or transposition error was made when calculating the transaction amount. - You altered the transaction amount after the transaction was completed without the consent of the cardholder. | - Review the invoice/receipt of the transaction and determine if an incorrect amount was charged. - If the claim is valid - respond to the Disputes Team confirming it was a valid customer dispute. - If a credit or reversal for the transaction has already occurred, provide documentation to support your claim; include the amount and the date it was processed. - If the correct amount has been charged, send the invoice/receipt of the transaction to the Disputes Team. |

For Card Not Present transaction disputes

| Dispute Reason | Description | Required actions |

|---|---|---|

| - Services not provided - Merchandise not received | A customer submitted a claim to their bank advising they did not receive, or only partially received goods they had purchased. This could be the result of: - The customer does not remember receiving the goods when they see the transaction on their credit card statement - Goods may have been stolen if left at the property in an unattended delivery; - The customer did not receive part of their order when delivered. - The store may have made an error and not delivered goods to the correct address. | - Review the transaction on your ecommerce platform to verify whether goods were delivered at the agreed date and location. - If the dispute was raised >120 days from the date the goods were purchased, provide the Disputes Team with the invoice/receipt of the transaction. Under the Card Scheme rules disputes need to be lodged within 120 days of the transaction date. - If the claim is valid, respond to the Disputes Team confirming that the charge back was valid. - Provide documentation confirming any credit or reversal for the transaction, specifying the amount and the date of processing. - If the goods were delivered as ordered, gather the signed delivery docket as confirmation of customer acceptance. Additionally, collect any evidence such as photos of the delivered goods at the specified location, GPS records, or email correspondence with the customer. - Alternatively, the customer may be contacted directly to resolve the dispute. If the customer no longer disputes the charge then obtain an email from the cardholder that states they no longer dispute the transaction and provide it to the Disputes Team. |

| - Not as described - Defective Merchandise | Customer has submitted a claim to their bank advising they did not receive the goods as ordered online. Specifically: 1. The cardholder received goods and or services that are different from the written description provided by the Merchant at the time of purchase. 2. The cardholder received damaged or defective goods and or services. | - Review the order details on your system against the delivery record to confirm the goods were correctly dispatched. If applicable check the model number on the order versus the model number of the goods dispatched. - Review the goods description on your website and validate against the goods being sold. - If the dispute is invalid provide copies of the above items such as screenshots from the website, description of goods and model numbers on the invoice. - For damaged goods or defective goods provide evidence confirming goods were delivered in proper order, and if applicable sale terms and conditions. Provide signatures if the customer confirmed receipt and acceptance of the delivery. |

| - No authorisation - Card Not Present - Fraud - Copy of authority Card absent - Fraud - Card Absent - No Cardholder Authorisation | Customer has submitted a claim to their bank advising they did not authorise the online transaction. This could be the result of: - A customer’s stolen credit card was used to make the purchase - The customer does not recognise the transaction on their credit card statement or remember making the online purchase. | - If applicable, provide proof that the disputed transaction was shipped to the same address as a previous transaction made by the card member that was not disputed. E.g. signed delivery docket confirming receipt of goods, GPS records of the delivery etc. - Evidence the cardholder has accessed and successfully verified the profile or account before the transaction date. - Cardholder's IP address and the geographical location of the device at the time of the transaction. - Cardholder's name and email address linked to customer profile or account. - See below on the Visa compelling evidence requirements for additional guidance. - Email conversations with the cardholder |

| - Duplicate Processing - Incorrect Amount | The cardholder has filed a dispute stating that a transaction has been processed more than once or the amount charged was incorrect. | - Review the customer’s transaction on your system to verify whether the transaction has been duplicated or the incorrect amount charged. - Obtain a full copy of the invoice/receipts for both of the disputed transactions. - If the claim is valid - respond to the disputes team confirming that the charge back was valid. - If a credit or reversal has already occurred, provide proof; include the amount and the date it was processed. |

“Compelling evidence” disputes process

Schemes have introduced new processes allowing merchants to provide additional types of evidence during pre-arbitration in cases where the cardholder took part in the transaction.

This can help to reduce chargeback losses related to ‘friendly fraud’ also known as ‘first party fraud’. ‘Friendly fraud’ is when a customer raises a chargeback claiming they don’t recognise the purchase, but then keeps the goods while the charge gets reimbursed.

If ‘compelling evidence’ is provided and flagged in the dispute response the card issuer must attempt to contact the customer with the new information and discuss why they feel a dispute is still valid.

This process applies to the following dispute categories raised in the dispute by the issuing bank:

- Dispute category 10.4 (Other Fraud – Card Absent Environment)

- Dispute category 4837 (No cardholder authorisation)

Allowable compelling evidence

- Evidence, such as photographic or email evidence to prove a link between the person receiving the merchandise or services and the Cardholder, or to prove that the Cardholder disputing the Transaction is in possession of the merchandise and/or is using the merchandise or services.

- For a Card-Absent Environment Transaction in which the merchandise is collected from the Merchant location, any of the following:

– Cardholder signature on the pick-up form

– Copy of identification presented by the Cardholder

– Details of identification presented by the Cardholder - For an Electronic Commerce Transaction representing the sale of digital goods downloaded from a Merchant’s website or application, description of the merchandise or services successfully downloaded, the date and time such merchandise or services were downloaded, and two or more of the following:

– Purchaser’s IP address and the device geographical location at the date and time of the Transaction

– Device ID number and name of device (if available)

– Purchaser’s name and email address linked to the customer profile held by the Merchant - Evidence that the profile set up by the purchaser on the Merchant’s website or application was accessed by the purchaser and has been successfully verified by the Merchant before the Transaction Date

– Evidence that the Merchant’s website or application was accessed by the Cardholder for merchandise services on or after the Transaction Date

– Evidence that the same device and Card used in the disputed Transaction were used in any previous Transaction that was not disputed - For a Transaction in which merchandise was delivered to a business address, evidence that the merchandise was delivered and that, at the time of delivery, the Cardholder was working for the company at that address. A signature is not required as evidence of delivery.

- For a Mail/Phone Order Transaction, a signed order form.

- For a Card-Absent Environment Transaction, evidence that 3 or more of the following had been used in an

undisputed Transaction:

– Customer account/login ID

– Delivery address

– Device ID/device fingerprint

– Email address

– IP address

– Telephone number - Evidence that the Transaction was completed by a member of the Cardholder’s household or family

- Evidence of one or more non-disputed payments for the same merchandise or service

- For a Recurring Transaction, evidence of all of the following:

– A legally binding contract held between the Merchant and the Cardholder

– The Cardholder is using the merchandise or services

– A previous Transaction that was not disputed

Scheme links

Mastercard Chargeback Guide: https://www.mastercard.us/content/dam/public/mastercardcom/na/global-site/documents/chargeback-guide.pdf

Visa Dispute Resolution Guide: https://www.visa.com.au/content/dam/VCOM/download/merchants/chargeback-management-guidelines-for-visa-merchants.pdf

Amex Chargeback Guide:

https://www.americanexpress.com/content/dam/amex/au/en/merchant/static/chargebackcodeguide.pdf

Updated over 1 year ago

For further assistance contact us here -

Dispute Resolution Team: [email protected]

Merchant Support Team: [email protected]